Calculated reporting period 31. Accounting codes

What codes for the billing and reporting period should be entered in the calculation of insurance premiums, which have been submitted to the Federal Tax Service since 2017? Where should I put the codes on the title page and in section 3? A table of codes with decoding, as well as a sample of codes on the title page, are in this reference material.

New calculation of contributions

Since 2017, the calculation and payment of insurance premiums have been controlled by the Federal Tax Service (Chapter 34 of the Tax Code of the Russian Federation). In this regard, starting from 2017, calculations of insurance contributions for compulsory pension (social, medical) insurance must be submitted to the tax inspectorates. At the same time, the form of calculation is completely new. The new form was approved by order of the Federal Tax Service of Russia dated October 10, 2016 No. ММВ-7-11/551. For the first time, reporting using the new form is required for the first quarter of 2017. Cm. " ".

Reporting and settlement periods according to the Tax Code of the Russian Federation

Since 2017, insurance premiums are regulated by the provisions of the Tax Code of the Russian Federation. Thus, in particular, Article 423 of the Tax Code of the Russian Federation defines the concepts of settlement and reporting periods for insurance premiums:

- the billing period is a calendar year;

- The reporting period is the first quarter, half year, nine months of the calendar year.

Period codes on the cover page of the calculation

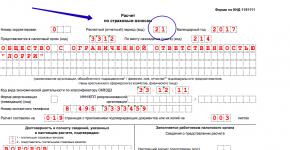

The calculation of insurance premiums, the form of which has been filled out since 2017 for the purpose of sending reports to the Federal Tax Service, includes, among other things, a title page.

On the title page, policyholders (organizations or individual entrepreneurs) need to fill in all fields except the section “To be completed by a tax authority employee.” On the title page there are fields “Calculation (reporting) period and “Calendar year”.

In the “Calculation (reporting) period” field you need to reflect the code of the period for which the calculation is being submitted. These codes are indicated in Appendix No. 3 to the Procedure for filling out a single calculation for insurance premiums. Here is a table of these codes with their explanation:

| Code | Name |

|---|---|

| 21 | 1st quarter |

| 31 | half year |

| 33 | nine month |

| 34 | year |

| 51 | 1st quarter during reorganization (liquidation) of the organization |

| 52 | half a year during reorganization (liquidation) of the organization |

| 53 | 9 months upon reorganization (liquidation) of an organization |

| 90 | year during reorganization (liquidation) of the organization |

In the “calendar year” field, indicate the year in which you submit your insurance premium calculation. Accordingly, if you submit a calculation, for example, for the 1st quarter of 2017, then filling out the title page and the billing period codes on it may look like this:

Please note that period codes have changed since 2017. Previously, when you submitted RSV-1 calculations, other codes were used:

- 3 – for the first quarter;

- 6 – for half a year;

- 9 – in nine months;

- 0 – per year.

Codes in section 3

Section 3 is personalized information for each individual. In this section you also need to show the code for the billing (reporting) period:

- 21 – for the first quarter;

- 31 – for half a year;

- 33 – in nine months;

- 34 – per year.

If the calculation is generated during the reorganization or liquidation of an organization, the codes will be as follows:

- 51 – for the first quarter;

- 52 – for half a year;

- 53 – in nine months;

- 90 – per year.

The value of field 020 of section 3 must correspond to the value of the “Calculation (reporting period (code)” field of the calculation title page.

Some of the information on the title page of the income tax return is indicated in encoded form. This includes the period for which the declaration was drawn up, the “number” of the Federal Tax Service for which the declaration is submitted, and some information about the taxpayer himself.

Period code in the income tax return

This code (Appendix No. 1 to the Procedure, approved by Order of the Federal Tax Service of Russia dated October 19, 2016 N ММВ-7-3/572@) allows tax authorities to determine for what specific period the payer submitted the declaration. Moreover, different codes are provided for ordinary organizations and responsible participants in a consolidated group of taxpayers (hereinafter referred to as the CTG).

| Tax/reporting period | Period code |

|---|---|

| For organizations (not KGN) submitting reports quarterly | |

| I quarter | 21 |

| Half year | 31 |

| 9 months | 33 |

| Year | 34 |

| For organizations (not KGN) submitting reports monthly | |

| One month | 35 |

| Two month | 36 |

| Three months | 37 |

| Four months | 38 |

| Five months | 39 |

| Six months | 40 |

| Seven months | 41 |

| Eight months | 42 |

| Nine month | 43 |

| Ten months | 44 |

| Eleven months | 45 |

| Year | 46 |

| For organizations that are responsible participants of the Group of Companies, submitting reports quarterly | |

| I quarter | 13 |

| Half year | 14 |

| 9 months | 15 |

| Year | 16 |

| For organizations that are responsible participants of the Group of Companies, submitting reports on a monthly basis | |

| One month | 57 |

| Two month | 58 |

| Three months | 59 |

| Four months | 60 |

| Five months | 61 |

| Six months | 62 |

| Seven months | 63 |

| Eight months | 64 |

| Nine month | 65 |

| Ten months | 66 |

| Eleven months | 67 |

| Year | 68 |

Special period code

In addition to codes for standard periods, there is a period code “50”. It must be supplied if an organization that is being liquidated or reorganized submits a declaration for the last tax period.

What other information is reflected by codes in the income tax return?

In the income tax return (approved by Order of the Federal Tax Service of Russia dated October 19, 2016 N ММВ-7-3/572@), the following information is subject to coding:

- name of the inspectorate to which the declaration is submitted. For example, if you submit reports to the Federal Tax Service of Russia No. 14 in Moscow, then the code “7714” is entered in the declaration;

- information about your affiliation with a specific inspection. Let's say your company, not being the largest taxpayer, submits an income tax return at the place of registration of the organization itself. In this case, you need to enter code “214” (“At the location of the Russian organization that is not the largest taxpayer”). And if, for example, you submit a declaration at the place of registration of your separate division, then the code “220” (“At the location of the separate division of the Russian organization”);

- data on reorganization/liquidation. For example, if the declaration is submitted by a company that is completing its activities, then “0” (“Liquidation”) is entered in the corresponding cell of the title page of the declaration;

- information about who signs the declaration: the payer himself (code “1”) or his representative (code “2”).

When insurance premiums were transferred under the control of tax authorities in 2017, a new chapter 34 was added to the Tax Code of the Russian Federation, regulating their calculation and payment procedure. It reveals the concepts that define both reporting periods and billing periods in relation to insurance premiums. In this article we will talk about the billing period for insurance premiums in 2018, and consider the payment deadlines.

Wherein:

- The reporting period is a quarter, half a year, etc.;

- and the calculated year is the calendar year.

During the billing period, accounting forms the basis for future accruals for insurance premiums. Each billing period is represented by four reporting periods, based on the results of which interim results can be summed up, as well as reporting can be submitted to the tax authority.

Calculation and reporting period for insurance premiums

The reporting period is recognized as:

- first quarter;

- half year;

- nine month;

By the way, for entrepreneurs who carry out their activities independently, without hiring employees and pay contributions only “for themselves,” there is no reporting period. In addition to entrepreneurs, such taxpayers include lawyers, notaries, etc. There are no specific deadlines for paying contributions during the year; they can pay the entire amount no later than December 31 of the accounting year.

If entrepreneurs have hired employees, they make deductions in the same manner as for organizations and submit reports at the end of each reporting period.

When an organization registered as a legal entity after the beginning of the year, the first billing period is set to the period from the date of registration to the end of the year.

Example 1. Continent LLC received a certificate of registration of a legal entity on April 13, 2017. Thus, the billing period for Continent LLC will be as follows: from April 13, 2017 to December 31, 2017. And the subsequent billing period will be equal to the full 2018 calendar year.

If the liquidation (reorganization) of a company occurs before the end of the calendar year, the end of the billing period will be the day the liquidation of the company or its reorganization is completed.

Example 2. Romashka LLC filed documents for liquidation. On November 18, 2017, Romashka LLC received an extract from the Unified State Register of Legal Entities. Accordingly, the billing period for insurance premiums will be as follows: from January 1, 2017 to November 18, 2017 inclusive.

In the event that the creation of a legal entity occurred after the beginning of the year, and liquidation or reorganization before its completion, the period from registration to liquidation should be recognized as the calculation period.

Example 3. Premier LLC received a registration certificate on April 5, 2017, and an extract from the Unified State Register of Legal Entities on liquidation on November 1, 2017. The calculation period for strass contributions will be as follows: from April 5, 2017 to November 1, 2017 inclusive.

Thus, in the billing period, at the end of each month, contributions are calculated based on the results of each month, based on the salary or other remuneration paid to employees. In this case, payments are taken into account from the beginning of the billing period to the end of the reporting month. The calculation is made taking into account the tariff rate, existing allowances or benefits to the tariff rate, subtracting the amount of the insurance payment calculated from the beginning of the billing period until the previous month.

Example 4. Continent LLC paid salaries and bonuses to employees:

- January 2017 – 120,000 rubles

- February 2017 – 140,000 rubles

- March 2017 – 130,000 rubles

At the end of January, the accountant calculated and paid contributions to compulsory pension insurance at a rate of 22%:

- 120,000 x 22% = 26,400 rubles

Based on the results of February, the accountant made the following calculation:

- (120,000 + 140,000) x 22% – 26,400 = 30,800 rubles

At the end of March, the accountant made the following calculation:

- (120,000 + 140,000 + 130,000) x 22% – (26,400 + 30,800) = 28,600 rubles

Calculation period for insurance premiums during organization reorganization

In the case of reorganization of a legal entity through merger, the end of the billing period ends on the day the reorganization is completed. And when a company merges with another, the first is recognized as reorganized from the moment an entry is made in the Unified State Register of Legal Entities (an entry on the termination of activities by merging a legal entity with another legal entity).

Reporting period codes

Let's look at the reporting period codes that need to be placed on the cover page of the calculation:

- 21 – first quarter

- 31 – half year

- 33 – nine months

- 34 – year

- 51 – first quarter during liquidation (reorganization)

- 52 – half a year during liquidation (reorganization)

- 53 – nine months during liquidation (reorganization)

- 90 – year during liquidation (reorganization)

Deadlines for submitting reports on insurance premiums

At the end of each reporting period, organizations are required to submit reports on insurance premiums to the tax authority. It is submitted no later than the 30th day of the month following the reporting period. That is, the report for the 1st quarter must be submitted no later than April 30. In the event that the last day of delivery falls on a weekend, the deadline is moved to the first next working day. So, in 2017, April 30 is a day off, and May 1 is a holiday, so the deadline for delivery is postponed to May 2.

The report is provided electronically or in paper form, it depends on the average headcount of the organization for the previous year. For example, if in 2016 it was more than 25 people, then the report will need to be submitted only in electronic form. Otherwise, the company will face penalties of 200 rubles. If the average headcount is less than 25 people, the company itself chooses the method of reporting. There will be no penalty for providing the report in non-electronic form.

Due dates for payment of contributions

Payment of contributions involves their monthly transfer in the form of mandatory payments. From 2017, contributions must be paid to the tax authorities. The deadline for payment is the 15th day of the month following the month for which accruals were made. So, if payment of contributions is planned for January 2017, then they must be transferred no later than February 15 of the same year.

Responsibility for violations in reporting

If, when checking the report, the inspector finds an error, the company will be notified of its elimination in electronic or paper form. At the same time, the period established for eliminating the error is 5 working days when sending an electronic notification and 10 when sending by mail. If the company for some reason ignores the inspector’s requirement, the calculation receives the status of unrepresented. For this, the company will be fined in the amount of 5% of the calculated insurance premiums for each month of delay.

The amount of the fine cannot exceed 30% of contributions, but it cannot be less than 1000 rubles.

The legislative framework.

Tax period code is a two-digit number that is used when submitting reports to the Federal Tax Service. The need for its use is due to machine processing of tax reporting. The code is entered in a special column and serves to determine the period for which the tax is paid. Different taxation systems require different codes. This is done on the basis of a code book.

How is the tax period determined: code in tax accounting

There are periods of time for which you need to report and provide a calculation of the tax base, they are called tax periods:

- month,

- quarter (from first to 4th),

- half-year (first, second),

The main reports are submitted based on the results of work for the year. The tax period is indicated in the declaration: code 34.

The quarters are assigned separate codes, the code begins with a two, followed by a number indicating the serial number of the quarter. For quarterly reporting, codes from 21 to 24 are used. So for the first quarter - code 21, tax period 22 for the second quarter, 23 for the third, tax period 24 for the fourth quarter.

Some taxpayers report monthly. It should be taken into account that different codes are provided for individual taxpayers and for a consolidated group. If payment is made by a consolidated group, then encryption is accepted from 13 to 15, from quarter to year. The periods from January to December are marked from 57 to 68.

Tax period when calculating income tax

When paying quarterly advances, the following coding is used: tax period 21 - first quarter, tax period 31 - first half of the year, 33 - nine months. Codes 35 to 46 indicate the months, starting from January and ending in December.

Tax period 50 is entered by taxpayers when filing reports before cessation of activity or reorganization. It is calculated from January 1 until the moment of actual liquidation, or from the moment of opening until the moment of liquidation, if the company existed for less than a year.

Tax period: code when calculating property tax

When reporting on this tax, it is not always necessary to submit interim reports; as a result, payment is made immediately for the year. The coding will be the same as for reporting on other taxes.

When preparing reports, code 21 is used (tax period - quarter), half-year - tax period - code 31, when calculating tax for 9 months, tax period 33 is indicated.

When liquidating an enterprise, codes 51, 52, 53 are used, they mean a quarter, half a year, 9 months.

Codes for reporting according to the simplified tax system

Organizations that are simplified submit a report to the Federal Tax Service on income once a year. An advance payment from the profit received is made quarterly. The year is divided into reporting periods in the same way as for income tax, but separate reporting for them is not required. The declaration indicates the standard period of one year, tax period 34.

For individual entrepreneurs, code 96 is used, which is used when terminating the activities of an individual entrepreneur for the final reporting period, and code 95, it is used for closing reporting in connection with a change in the taxation regime.

Tax period codes for UTII

Reporting is carried out quarterly, using the following designations:

- Quarter - 21,

- tax period 2nd quarter – 22,

- tax period 23 – for the third quarter,

- tax period code 24 – used when reporting for the fourth quarter.

On the title page of form 6-NDFL, a number of codes are indicated in the calculation header. One of them - “Representation period” - is a field of two cells (cells). What codes there are for filling out this field, where to get them and when exactly to indicate, read our article.

Submission period - code in 6-NDFL: what it looks like

The code, which indicates the period for submitting the calculation, consists of a two-digit code. A separate field is allocated for it in the very center of the calculation, immediately below the name of the form.

To make it clearer what we are talking about, we have provided a fragment of the completed 6-NDFL report (title page).

Submission period - code in 6-NDFL: where to get the values

The codes for submission periods are given in Appendix No. 1 to the Procedure for filling out the form (Order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450@ as amended dated January 17, 2018).

The values in the specified application are presented in table form.

Submission period - code in 6-NDFL: what values are there

Form 6-NDFL is submitted to the Federal Tax Service by all tax agents for personal income tax quarterly during the year and at the end of the year. In this case, the form is filled out as a whole with an accrual total from the beginning of the year. This is exactly how Section 1 of the form is drawn up. Section 2 provides indicators only for the last three months of the reporting (tax) period. For example, if calculated for 9 months, these will be figures for July-September.

During the year, the form is submitted within a month following the results of the reporting period. At the end of the year - until April 1 inclusive (paragraph 3, paragraph 2, article 230 of the Tax Code).

Accordingly, four presentation period codes have been identified:

- for reporting for the 1st quarter - value 21;

- for half a year (6 months) (2nd quarter) - 31;

- 9 (nine) months (3rd quarter) - 33;

- year (4th quarter) - 34.

The numbers, as it is not difficult to notice, are increasing.

For a situation where a company is in the process of reorganization (liquidation), the codes are their own. These are the corresponding values: 51, 52, 53 and 90.

As a general rule, we repeat, codes 21, 31, 33 and 34 are indicated - depending on the reporting period.

We have collected all the values for all possible cases in our own table.

Codes for submission periods of form 6-NDFL in 2018 - table

Submission period - code in 6-NDFL: how to choose a value

The purpose of the code is to indicate the period for which the report is provided. The year for which reporting is submitted is indicated in numbers in the adjacent field. That is, in 2018 it will be the value of 2018.

In total, over the course of a year, an operating company will have sequentially completed calculations with all presentation codes.

If the company is newly registered, then code 21 is not necessarily entered into the calculation for the first time. Thus, for companies registered in April 2018, the first calculation in Form 6-NDFL will be the calculation for the six months. Accordingly, you will need to enter code 31 (for the 2nd quarter) in the first calculation.

If at the beginning of the year there were transactions for which your company acted as a tax agent, then the report must be submitted by the end of the year, even if the activity is no longer carried out. Therefore, in this case, all available codes for submitting form 6-NDFL are also used.

For liquidated (reorganized) companies, in the line “Representation period (code)” a code corresponding to the time period from the beginning of the year in which the liquidation (reorganization) occurred until the day the liquidation (reorganization) was completed. For example, when a company is liquidated in September 2018, the code “53” is entered in the specified line. Other special lines of the form provided for the liquidation (reorganization) procedure are also filled out. For more precise explanations, please refer to the Procedure for filling out the form.

Sample of completing the “submission period” code in 6-NDFL

Code at the location of registration in 6-NDFL: what happens if you make a mistake

For each payment with false information, a fine of 500 rubles is provided. But: if you discover an error and submit an amendment before the tax authorities identify the inaccuracy, there will be no sanctions (Article 126.1 of the Tax Code).

In the case of confusion in the code for the submission period, the Federal Tax Service may well consider that the report for a specific current period has not been submitted at all. In this case, the fine for the tax agent is 1000 rubles. for each full or partial month from the day established for submitting the calculation to the inspection (clause 1.2 of Article 126 of the Tax Code). The tax authorities calculate the time of delay from this day until the date when the 6-NDFL is submitted. True, inspectors have the right to a fine only for 10 working days (this is the time for a desk audit of the report).

For failure to submit 6-NDFL, inspectors also have the right to block the tax agent’s account. To do this, the auditors have the same 10 days from the date when the deadline for submitting the calculation expired (clause 3.2 of Article 76 of the Tax Code, letter of the Federal Tax Service dated 08/09/2016 No. GD-4-11/14515).

In order not to cause such unpleasant consequences as described above, it is in the interests of the tax agent himself to be extremely careful when filling out the calculation header. If you type out the report yourself on a computer, copying previous calculations, be sure to double-check all the values. And an indispensable point for control is the field with the submission period code 6-NDFL.

Inspectors may impose a fine due to any error in the calculation in Form 6-NDFL. In some situations, they reduce the fine due to the presence of mitigating circumstances (clause 1 of Article 112 of the Tax Code). These are cases when the tax agent, due to an error (letter of the Federal Tax Service dated 08/09/2016 No. GD-4-11/14515):

- did not underestimate the tax;

- did not create adverse budgetary consequences;

- did not violate the rights of individuals.

Note: if an error is recognized, not only the tax agent company, but also its authorized officials may be fined. For example, a director or chief accountant of a company. The amount of possible personal sanctions varies from 300 to 500 rubles. (Article 15.6 of the Administrative Code).